$VIX Futures Premium Indicator

"The Big (Volatility) Short" trade is setting up once again.

A number of years ago, we introduced a $VIX futures premium indicator, which we called VOLFUTA. It is a composite of the premium on the front-month and second-month $VIX futures, weighted appropriately as in the $VIX formula. When this premium is large, it means that the futures are subject to a great deal of “time decay” as time passes, and the futures premium wastes away. That is the case most of the time and has led traders over the years to attempt to be short the Volatility ETFs that mirror this – VXX, in particular. Alternatively, one could be long the Inverse $VIX ETF (SVXY).

We termed this “THE BIG (VOLATILITY) SHORT.”

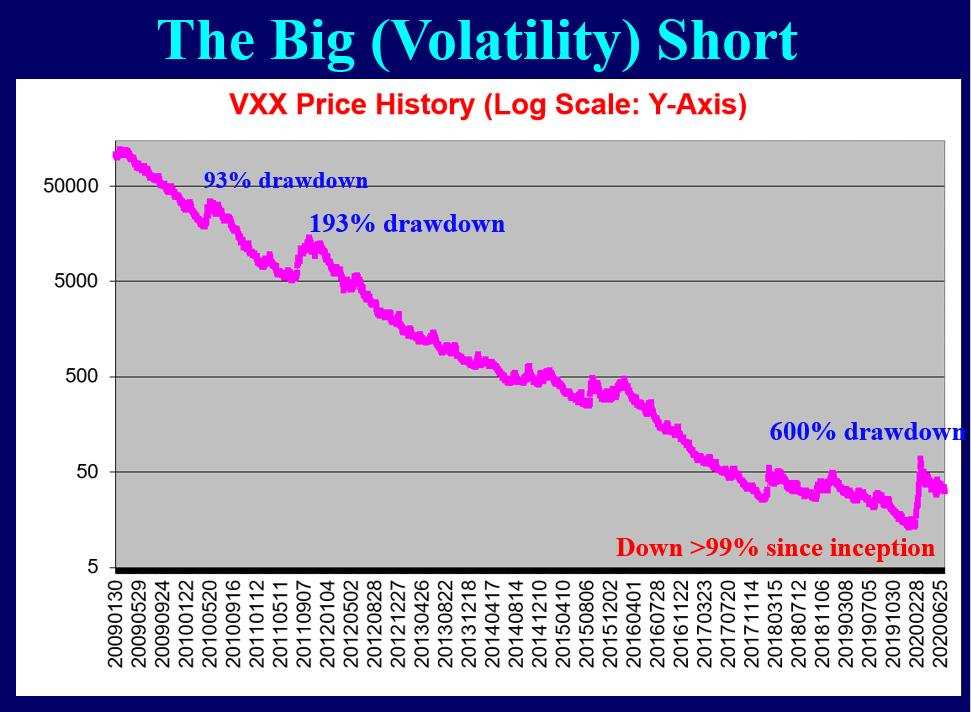

The graph below shows the devastating effect of buying VXX and holding. The time decay of the premium in the $VIX futures is overwhelming. Yes, there are times when it works, and they are marked here as “drawdowns” because – if one were short, that’s what they would be. Those drawdowns would have wiped you out as a short – and it happened to the previous short volatility ETF (XIV).

The graph above was from the original article and has been used in many of our presentations to illustrate this concept. The graph below brings it up to date, showing the data since the beginning of 2018 only.

Keep reading with a 7-day free trial

Subscribe to The Option Strategist Substack to keep reading this post and get 7 days of free access to the full post archives.